Last Month in the Markets: November 1st – 30th, 2023

What happened in November?

November was an exceptionally strong month for financial markets, driven by a growing sentiment of substantial rate cuts in 2024 and further fueled by the smaller than expected US Treasury debt issuance. This included a strong performance in both US investment grade and global government bonds.

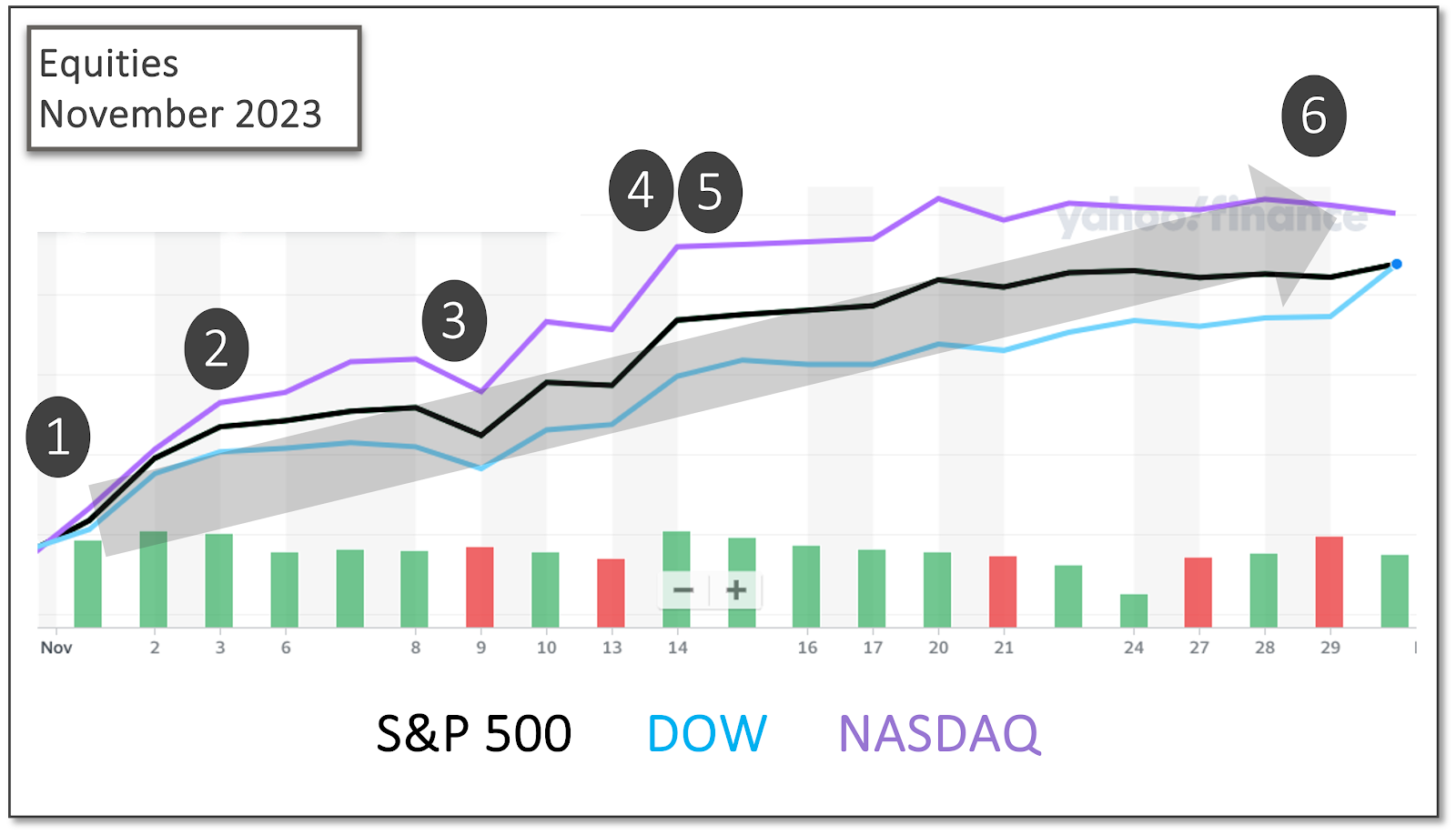

For Equities, the major American indexes were led by the NASDAQ, with a 10.5% increase, the Dow and S&P 500 rose nearly 9%. The Euro Area, represented by the Euro Stoxx 50 index, closely followed behind with a return of just below 8%, followed by the TSX and Japanese markets, gaining just under 6%. The Chinese and UK markets lagged, ending flat to slightly negative. International stock performance was helped by a depreciation in the US dollar, showing its counter cyclical nature and reflecting the rate cutting sentiment.

While November saw a temporary calming of geopolitical conflict, gold continued to perform well, reflecting that underlying tensions remain. President Biden and Chinese President Xi met in San Francisco ahead of the Asia Pacific Economic Cooperation summit to thaw relations between the two countries. A U.S. government shutdown was averted mid-month after passing a bipartisan spending and debt bill. The war between Hamas and Israel paused to allow humanitarian aid into Gaza, and a hostage/prisoner exchange.

Other commodities were more muted, industrial metals were flat over the month and oil fell on short term supply and demand dynamics. The supply disruption from the Israel and Hamas war cooled over the month and traders turned their attention to slowing demand concerns while reacting skeptically to the voluntary oil output cuts agreed on by OPEC+. iea.org

The month concluded with positive inflation news from the U.S., further increasing analyst expectations that the Federal Reserve could began cutting rates in 2024.

Here were the key events this month:

- November 1st

The U.S. Federal Reserve held the federal funds rate within the range of 5.25 to 5.5%. Although no promises of rate reductions were offered, the continuation of the rate pause caused a positive reaction in equity markets. North America stocks rose on the news after several week of poor performance. Fed release CNBC equities and Fed

- November 3rd

The Bureau of Labor Statistics reported that nonfarm payroll had risen by 150,000 in October, and the unemployment rate rose 0.1% to 3.9%. Each of the major worker categories saw little change in unemployment rates, as a total of 6.5 million Americans were unemployed. BLS release

- November 9th

Federal Reserve Chair, Jerome Powell, stated at an International Monetary Fund meeting that interest rates may not be high enough, yet, to bring inflation back to the 2% target, again demonstrating the sensitivity of markets to interest rate speculation. AP and Powell

- November 14th

U.S. consumer inflation was little changed in the month of October after increasing 0.4% in September. Over the past twelve months the all-items Consumer Price Index increased 3.2%, down from September’s year-over-year inflation of 3.7%. The rise in the price of shelter was offset by the decline in the price of gasoline. U.S. equity indexes rose 1.5 to 2.5% and the TSX jumped 1.6% for the day. BLS release CNBC and CPI More CNBC and CPI

- November 15th

Producer prices fell 0.5% in October, after rising 0.4% in September. This is the largest, monthly price reduction for the Producer Price Index since April 2020, when it fell 1.2%. BLS PPI release

After the U.S. House of Representatives passed another spending bill the day before, the Senate voted 87-11 to end the third and latest fiscal standoff ahead of a deadline. CNN and US Govt

- November 30th

On the 30th, the Bureau of Economic Analysis released its Personal Consumption and Expenditures (PCE) price index. The PCE is the Federal Reserve’s primary inflation indicator, in part because it accounts for changes in behaviours like choosing lower priced alternatives (e.g., generic versus name brands). For the most recent period, October, the PCE rose 0.1%, and 3% from a year ago, matching analyst expectations. CNBC and PCE BEA PCE release NYTimes and PCE

What’s ahead for December?

The Bank of Canada released its interest rate decision on December 6th, holding its policy rate at 5% and choosing to continue with quantitative tightening, stating that it is seeing signs of economic weakening, decreasing inflation and labour market easing. The next interest rate announcement from the Federal Reserve is scheduled for December 13th. Bank of Canada

The muted PCE measured inflation news from the Bureau of Economic Analysis provides conviction that rate cuts are increasing likely next year, which has been reflected in the markets. The extent of the economic slowdown that will accompany this, however, is still up for debate.

Markets are currently reflecting the view of a soft-landing scenario. As economies have shown astounding resiliency because consumer spending, especially in the US. However, we are now amid the most restrictive monetary policy since the 1980s. Savings is quickly being exhausted, and more household income will need to be spent on debt repayment as mortgage and loan rates renew to the current, higher market rates. The tightening of lending conditions will also cause a slow down in business investment, which we haven’t seen the full effect of yet. Blackrock

While during November the unemployment rate was little changed, we are seeing loosening dynamics as voluntary quits fell and companies reduced hiring. Labour market loosening has been a focus for Central Banks, which will make avoiding a recession tricky, as a rising unemployment rate has long been a recession indicator. Sahm Rule

Central Banks will need to time the easing of policy at just right time to provide a soft landing, a tough expectation. Especially since they underestimated the inflationary pressures created during the pandemic and are set on not being taken off guard again. There is a large risk they will keep rates too high for too long. This leads us to continue our view of overweighting fixed income and keeping our equity holdings tilted towards quality and defensive names.

Qopia Investments is a trade name of Aligned Capital Partners Inc. (ACPI). ACPI is regulated by the Investment Industry Regulatory Organization of Canada (www.iiroc.ca) and a Member of the Canadian Investor Protection Fund (www.cipf.ca). Qopia Investments is registered to advise in securities and mutual Funds to clients residing in Alberta, Ontario, Saskatchewan, and British Colombia. This publication is for informational purposes only and shall not be construed to constitute any form of investment advice. The views expressed are those of the author and may not necessarily be those of ACPI. Opinions expressed are as of the date of this publication and are subject to change without notice and information has been compiled from sources believed to be reliable. This publication has been prepared for general circulation and without regard to the individual financial circumstances and objectives of persons who receive it. You should not act or rely on the information without seeking the advice of the appropriate professional.

Investment products are provided by ACPI and include, but are not limited to, mutual funds, stocks, and bonds. Non-securities related business includes, without limitation, fee-based financial planning services; estate and tax planning; tax return preparation services; advising in or selling any type of insurance product; any type of mortgage service. Accordingly, ACPI is not providing and does not supervise any of the above noted activities and you should not rely on ACPI for any review of any non-securities services provided by

Investment products are provided by ACPI and include, but are not limited to, mutual funds, stocks, and bonds. Non-securities related business includes, without limitation, fee-based financial planning services; estate and tax planning; tax return preparation services; advising in or selling any type of insurance product; any type of mortgage service. Accordingly, ACPI is not providing and does not supervise any of the above noted activities and you should not rely on ACPI for any review of any non-securities services provided by Qopia Financial.

Any investment products and services referred to herein are only available to investors in certain jurisdictions where they may be legally offered and to certain investors who are qualified according to the laws of the applicable jurisdiction. The information contained does not constitute an offer or solicitation to buy or sell any product or service. Past performance is not indicative of future performance, future returns are not guaranteed, and a loss of principal may occur. Content may not be reproduced or copied by any means without the prior consent of the author and ACPI.

Disclosure of commissions in mutual funds in accordance with NI 81-102 (15):“Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated”.