Last Month in the Markets: January 2nd – 31st, 2024

What happened in January?

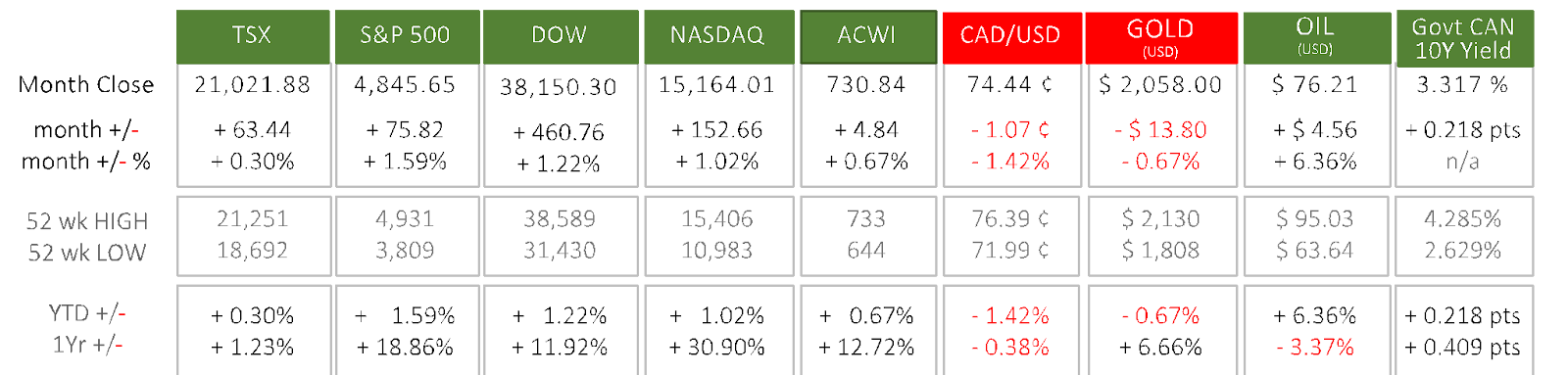

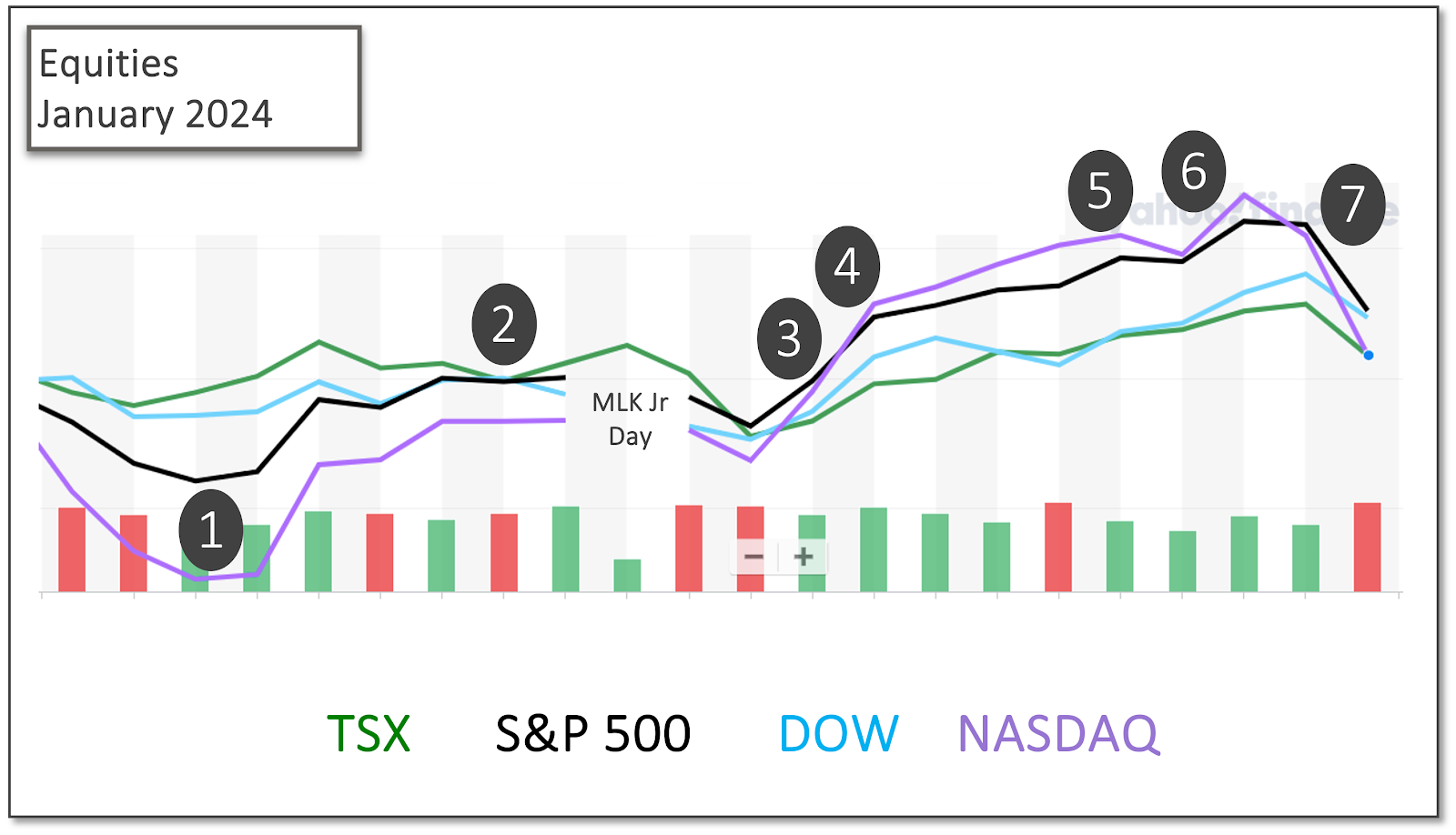

The 2023 narrative continued over the month of January as large cap US stocks, led by the tech giants, progressed in their dominant position over the rest of the market. The S&P 500, with a roughly 20% exposure to these companies, started off the month hitting a new high before detracting as a strong U.S. jobs report simmered hopes of a Fed rate cut late in the month. Shortly afterward, reports showing inflation progress helped facilitate the S&P 500 and Dow reach new all-time highs. In contrast, the Russell 2000, which is an index comprising of US small cap companies, didn’t participate in the rally, ending the month down 3.9%. With Canada showing less economic resilience than the US, the TSX finished the month with a small gain.

Internationally, Chinese stocks continued their losing streak and performed exceptionally poorly, with markets expecting that government stimulus measures won’t generate any meaningful economic recovery. This dragged down industrial metals and emerging markets. European markets squeaked out a small gain, but it was offset to a slightly negative return from an American perspective, as the Euro depreciated relative to the USD. The notable performance for the month was that in Japanese equities, with the Nikkei 225 rising over 8.5%. This was due to sentiment of improved corporate governance, a strong computer chip sector, and the depreciation of the Yen relative to the USD, causing foreign investment interest. reuters

Oil rose over 6% due to a relapse of significant geopolitical tensions in the middle east.

Long term bond yields staged a retracement from their huge decrease at the end of 2023, with continued US economic resilience causing the market to backtrack on its aggressive bet of large rate cuts. The annualized Consumer Price Index for December sits at nearly 4% in Canada and 3.5% in the US, which are well below previous levels but still not at central bank targets.

(source: Bloomberg https://www.bloomberg.com/marketsand ARG Inc. analysis)

Here were the key events of the month:

- January 5th

The US nonfarm payroll employment increased 216,000 in December, exceeding analyst expectations and adding to inflation risk. The unemployment rate of 3.7% was based on 6.3 million unemployed in December. One year ago, the unemployment rate was 3.5% and number was 5.7 million. BLS release CNBC Financial Post and jobs CNBC and jobs and rates

- January 11th

The US Bureau of Labor Statistics (BLS) released the Consumer Price Index (CPI) for December, and year-over-year inflation for 2024. Consumer prices rose 0.3% in December, up from 0.1% in November. Over the past 12 months, the all-items index increased 3.4%, compared to 3.1% at the end of November. Over the past year the Core CPI decreased slightly to 3.9% from 4.0% at the end of November. BLS CPI release

- January 18th

After a market correction related to US employment and inflation data, the influence high levels of government spending have on keeping the US economy resilient was highlighted as US equities jumped when Congress approved another stop-gap spending bill to keep the federal government operating until the beginning of March. The S&P 500 and Dow set a new all-time high and this was the eleventh positive week for US indexes out of the last twelve. WaPo and spending bill

- January 19th

The Canadian Consumer Price Index (CPI) rose 3.4% on a year-over-year basis in December, after 3.1% in November. Increases in gasoline, fuel oil, airfares, passenger vehicles, rent and groceries contributed to the increase in inflation. For the month, the CPI fell 0.3% in December, after a 0.1% gain in November. CPI Annual Review StatsCan and CPI CBC and CPI CityNews

- January 24th

The Bank of Canada held its policy interest rate, the overnight rate, steady at 5%, and the Bank Rate at 5.25%. It also continued its program of quantitative tightening. They stated their anticipation of inflation slowing in 2024 but are waiting to see further confirmation. BoC release and MPR

- January 25th

Reports were released showing quarterly and annual Gross Domestic Product (GDP) growth. The American economy grew faster than expected for the 4th quarter and 2023, and inflation cooled for December and in 2023, according to the Bureau of Economic Analysis. In the fourth quarter GDP increased at a 3.3% annualized rate, and 2.5% for 2023. Strong consumer and government spending was the reason.

The Personal Consumption and Expenditure price index (PCE) rose 0.2% in December and 2.9% for 2023. Including food and energy, headline inflation rose 2.6% annually at the end of December. The annualized rate of inflation is approaching the Fed’s low-term average goal of 2%.

The trend seen of higher than expected GDP growth and lowering inflation is defying the economic logic of the US experiencing a recession from tight monetary policy. BEA GDP release CNBC and GDP BEA PCE release CNBC and PCE

- January 31st

On the last afternoon of the month, the Federal Reserve released its monetary policy update. Interest rates and the course of quantitative tightening were held steady, which matched market and analyst expectations. The next Fed interest rate announcement is scheduled for March 20th.

The Fed released an accompanying statement suggesting they believe the U.S. economy is performing well enough to not need an easing of monetary policy and lower rates could risk re-igniting inflation. CME FedWatch Fed release and presser

What’s ahead for February and beyond?

The next two interest rate announcements from the Bank of Canada are March 6th and April 10th as well as March 20th and May 1st for the Federal Reserve. As February begins, markets have been retracting their view of a March 20th rate cut from the Fed, with a strong employment data release on February 2nd and Fed Chair Jerome Powell leaning into the statement released the end of January, stating on a February 4th 60 minutes interview that “it’s not likely that the committee will reach that level of confidence [to cut rates] in time for the March meeting.” wsj

In Canada, employment growth has slowed. The last announcement showed that new job creation had ceased, as well as immigration and labour market participation have driven the unemployment rate higher.

The US the jobs market remains strong, but cracks continue to show, the most recent being the accelerating pace of lay offs in the temporary job market and full-time job numbers contracting. However, due to this resilience, there is a case that the Bank of Canada will start lowering rates before the Fed does. It is not a certainty for either March or April, but consensus is growing that by June, Canadian rates will begin to come down. bnnbloomberg CBC and BoC rates

While global economies continue in flux, we are keeping our asset allocation steady, with a tilt towards income and defensive equities, as well as a focus on quality holdings.

Qopia Investments is a trade name of Aligned Capital Partners Inc. (ACPI). ACPI is regulated by the Investment Industry Regulatory Organization of Canada (www.iiroc.ca) and a Member of the Canadian Investor Protection Fund (www.cipf.ca). Qopia Investments is registered to advise in securities and mutual Funds to clients residing in Alberta, Ontario, Saskatchewan, and British Colombia. This publication is for informational purposes only and shall not be construed to constitute any form of investment advice. The views expressed are those of the author and may not necessarily be those of ACPI. Opinions expressed are as of the date of this publication and are subject to change without notice and information has been compiled from sources believed to be reliable. This publication has been prepared for general circulation and without regard to the individual financial circumstances and objectives of persons who receive it. You should not act or rely on the information without seeking the advice of the appropriate professional.

Investment products are provided by ACPI and include, but are not limited to, mutual funds, stocks, and bonds. Non-securities related business includes, without limitation, fee-based financial planning services; estate and tax planning; tax return preparation services; advising in or selling any type of insurance product; any type of mortgage service. Accordingly, ACPI is not providing and does not supervise any of the above noted activities and you should not rely on ACPI for any review of any non-securities services provided by

Investment products are provided by ACPI and include, but are not limited to, mutual funds, stocks, and bonds. Non-securities related business includes, without limitation, fee-based financial planning services; estate and tax planning; tax return preparation services; advising in or selling any type of insurance product; any type of mortgage service. Accordingly, ACPI is not providing and does not supervise any of the above noted activities and you should not rely on ACPI for any review of any non-securities services provided by Qopia Financial.

Any investment products and services referred to herein are only available to investors in certain jurisdictions where they may be legally offered and to certain investors who are qualified according to the laws of the applicable jurisdiction. The information contained does not constitute an offer or solicitation to buy or sell any product or service. Past performance is not indicative of future performance, future returns are not guaranteed, and a loss of principal may occur. Content may not be reproduced or copied by any means without the prior consent of the author and ACPI.

Disclosure of commissions in mutual funds in accordance with NI 81-102 (15):“Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated”.